Life Interest Trusts in BC: Essential Considerations and Legal Framework

Life interest trusts are a valuable estate planning tool in British Columbia, often used to provide ongoing support for a surviving spouse or family member while preserving the capital of the estate for future beneficiaries.

These trusts allow one individual to benefit from the income or use of certain assets during their lifetime, with the remaining interest passing to others after their death.

This article explores the essential considerations and legal framework surrounding life interest trusts in BC, helping you determine whether this option aligns with your estate planning goals.

Overview of Life Interest Trusts in BC

Life interest trusts play a vital role in estate planning in British Columbia. They allow you to protect assets and provide income for selected beneficiaries, while also deciding who will receive the property after the initial beneficiary’s death.

Definition and Purpose

A life interest trust, also called a life estate trust, lets you choose a person (the life tenant) who will benefit from certain assets for the rest of their life. During this time, the life tenant can get income from the trust or use the trust property, depending on how the trust is set up. After the life tenant dies, the remaining assets go to another person or group (the remainder beneficiaries).

The main purpose of these trusts is to give ongoing support to a spouse, partner, or another family member without giving them outright ownership. This helps preserve assets for future generations and often ensures that your wishes for the final distribution of property are respected. These trusts can also provide protection for minor children or beneficiaries with disabilities, as explained by the Government of BC.

Key Features

Life interest trusts in BC have several important features to consider. Only the life tenant can get the income or benefit from the trust property during their lifetime. They usually cannot change the ultimate beneficiary or sell the trust assets, unless the trust specifically allows it.

The trust is managed by a trustee, who is responsible for following the terms you set out in the trust deed. The trustee must balance the needs of the life tenant with the interests of the remainder beneficiaries.

Often, these trusts are used to manage real estate, investments, or other assets that you want protected and transferred smoothly after the first beneficiary’s death.

Types of Life Interest Trusts

There are several common types used in British Columbia. Spousal trusts provide income or benefit to a surviving spouse during their life. Joint spousal trusts let both spouses benefit while either is alive, with the assets passing to others when both have died.

Alter ego trusts are for people over 65. You, as the settlor, keep full benefit during your lifetime, and the trust then names who receives the assets after you pass away. These are often used to avoid probate and protect privacy.

Each type serves different estate planning goals. You may choose the structure that fits your family’s needs. This choice can affect taxes, eligibility for government assistance, and how assets are managed and distributed.

Legal Framework and Legislation

Life interest trusts in British Columbia must follow specific rules set out by provincial laws. These rules define how life interest trusts are created, managed, and varied, ensuring that the interests of all parties are protected.

Applicable Laws in British Columbia

The main law for life interest trusts in British Columbia is the Trust and Settlement Variation Act. The Act allows the Supreme Court to make decisions about trusts when needed, especially if they involve land or legal life interests.

Under this law, if a person has a legal life interest in land, they are seen as holding the land in trust for themselves and anyone else who may inherit later. The court may change trust terms to better protect the rights of those with future interests.

The Act helps solve problems that may come up when a trust affects different generations. It gives the court the power to approve changes, so the trust can still meet the needs of everyone involved. For more information, see the full text of the Trust and Settlement Variation Act.

Role of the Wills, Estates and Succession Act

The Wills, Estates and Succession Act (WESA) sets out the rules for making wills and handling estates, including trusts set up by a will. If you are creating a life interest trust through your will, WESA will affect how that trust works.

WESA helps make sure that a person’s wishes about their estate, including any life interest trust, are followed. It covers when a trust starts, who can benefit from it, and how it is managed after death.

This law also gives guidance on what happens if there are problems with the will or trust, such as mistakes or unclear terms.

Establishing a Life Interest Trust

A life interest trust in British Columbia lets you provide a designated person with the right to use assets, often real estate or investments, for their lifetime. This kind of trust can be a helpful tool for estate planning, tax management, and long-term family security.

Requirements for Creation

To create a life interest trust in BC, you must have a clear intention to form the trust and properly document the arrangement. Usually, this requires writing a trust deed or including trust terms in your will. The deed must clearly state the assets, the person receiving the life interest, and any other beneficiaries.

For some types of life interest trusts, such as an alter ego trust or a joint partner trust, the person who establishes the trust (the settlor) must be at least 65 years old. Other trusts, like spousal trusts, do not require a minimum age. You also need to follow the rules in the Trust and Settlement Variation Act when the trust involves real estate or if you seek the court’s approval for changes. Notaries in BC cannot prepare wills that create life estates or trusts; only lawyers can do so.

Parties Involved

Life interest trusts have specific parties involved:

Settlor: The person who creates the trust and transfers property into it.

Trustee(s): Individuals or trust companies responsible for managing the assets according to the trust terms.

Life Tenant (Beneficiary): The person who gets the right to use or benefit from the trust assets during their lifetime.

Remainder Beneficiaries: Those who will inherit the trust assets after the life tenant passes away.

All parties play distinct roles, and clear lines of responsibility must be established. The trustee has a legal duty to act in the best interest of both the life tenant and the remainder beneficiaries.

Trust Terms and Conditions

The trust deed or will must set out the terms and conditions in detail. These terms should explain what assets are included, how those assets are to be managed or used, and what rights the life tenant will have. For example, a life tenant may have exclusive use of a home or receive all income from investments but may not be allowed to sell the assets.

Rules about who pays for upkeep, taxes, and insurance should also be clear. The trust should address what happens if the life tenant moves, cannot look after the property, or passes away. Properly drafted terms help prevent confusion and conflict between beneficiaries.

Life interest trusts often end when the life tenant dies, at which point the assets pass to the remainder beneficiaries. Details about the transfer process and timing should be included to ensure the trust is administered efficiently.

Duties and Powers of Trustees

If you are appointed as a trustee of a life interest trust in British Columbia, you must follow strict legal duties. You are also given certain powers to manage and protect trust assets on behalf of the beneficiaries.

Fiduciary Responsibilities

Your main duty as a trustee is to act in the best interest of the beneficiaries at all times. This is called a fiduciary responsibility. You must be honest, avoid conflicts between your personal interests and the trust’s interests, and treat each beneficiary fairly.

You must follow the terms set out in the trust document. If you fail to do so, you may be held personally responsible for any losses to the trust. It is important not to favour one beneficiary over another unless the trust specifically tells you to.

You should keep detailed records of all trust accounts, payments, and decisions. Open communication with beneficiaries is also required. You must keep them informed about important matters, such as trust income or changes in trust management.

Asset Management

You have the power and duty to manage, invest, and protect the trust's property. Investments must be made carefully and thoughtfully. In British Columbia, you must act as a "prudent investor" and assess the risks and benefits as a reasonable person would in similar circumstances.

You may appoint professional agents, like solicitors or bankers, for help with complex matters or to receive money on the trust’s behalf. However, you remain responsible for the overall management.

Typical trustee powers include:

Collecting income from trust property

Distributing payments as required

Keeping assets secure and insured

Making investment decisions

Any action you take should aim to protect and support the trust’s purpose and the interests of the beneficiaries.

Rights of Life Interest Beneficiaries

A life interest beneficiary has the right to use or benefit from the trust property during their lifetime, but their control is not absolute. Specific legal rules and duties apply, shaping the extent of your rights and the circumstances under which those rights can end.

Entitlements and Limitations

As a life interest beneficiary, you have the right to live in or receive income from the property covered by the trust. For example, if the property is a house, you may occupy it exclusively or collect rental income during your lifetime.

Your rights are often subject to certain conditions. You are usually responsible for regular expenses such as utilities and routine maintenance. However, larger costs like property taxes, insurance, and major repairs may be the responsibility of the remainder beneficiaries or the trust, depending on the trust terms and court orders.

Limitations include that you cannot sell, give away, or leave the trust property to someone else in your will. Your rights are personal and end with your death. You must also take reasonable care of the property and not allow it to lose value beyond normal use.

Termination of Life Interest

Your life interest ends upon your death, at which point the property passes to the remainder beneficiaries named in the trust or will. After your life interest is extinguished, you no longer have any claim or control over the asset.

A life interest can also end if you give up your rights voluntarily, sometimes called "surrendering" your interest in the trust. In rare cases, a court may order the termination of a life interest if there is legal cause, such as the destruction of the property or a breach of trust duties.

When the life interest terminates, the remainder beneficiary or beneficiaries gain full ownership and control over the property. This transfer is automatic; it does not require probate or court intervention unless the trust terms or local laws require it. For property in British Columbia, the law treats the life tenant as holding the land in trust for themselves and future beneficiaries, as described in the Trust and Settlement Variation Act.

Tax Implications for Life Interest Trusts in BC

Life interest trusts have specific tax rules in British Columbia. You should be aware of how income is handled and what happens when trust property changes ownership or when beneficiaries pass away.

Income Tax Treatment

You are taxed on the income earned by a life interest trust in a particular way. The income that a trust earns from its property—such as rent, interest, or dividends—must be reported, and the trust is often required to file a T3 return each year.

In many cases, the beneficiary with the life interest (for example, you or your spouse) is taxed on the income from the trust, since the law deems the income to belong to them. This means you must add this income to your personal return for the year. If the trust distributes income to more than one beneficiary, each one is responsible for paying tax on their share.

The trust itself may also have to pay taxes if it keeps any income rather than distributing it. Not filing the proper tax forms or not reporting the right amount can result in penalties and interest charged by the Canada Revenue Agency.

Deemed Disposition Rules

When you set up a life interest trust, there are special rules that affect how capital gains are taxed. At certain times, the trust property is treated as if it was sold at its fair market value, even if no actual sale happens. This is called a "deemed disposition."

A deemed disposition usually happens at the death of the last life interest beneficiary or after 21 years from the trust’s creation. When this occurs, the trust must pay tax on any increase in the value of its property since it was acquired. You should plan for this possible tax bill, especially if valuable assets are held in the trust.

This rule prevents trust property from avoiding taxes on capital gains for too long. It is important to keep accurate records of the adjusted cost base to calculate these gains correctly.

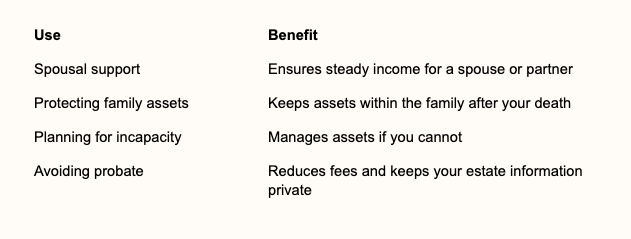

Common Uses and Practical Applications

You can use life interest trusts in British Columbia for several reasons. One of the main uses is to provide income and support for a spouse or partner during their lifetime while protecting the capital for other beneficiaries, such as children, after the first person passes away. This method helps you keep assets within your family across generations.

Life interest trusts are also helpful if you want to plan for incapacity. The trust can manage your assets if you are no longer able to make decisions, avoiding the need for a court process or public involvement.

Many people use these trusts to help reduce probate fees and avoid the probate process. Assets held in a trust do not go through probate on death, which can save time and costs for your heirs. This also helps keep the details of your estate private.

The following table outlines some common uses of life interest trusts:

Dispute Resolution and Legal Challenges

Disagreements may happen if individuals feel a life interest trust in British Columbia was set up unfairly or is being managed improperly. Understanding your options can help you make informed decisions when dealing with trust disputes.

Contesting a Life Interest Trust

You may contest a life interest trust if you believe the trust is invalid or was created under suspicious circumstances, such as undue influence, fraud, or a lack of mental capacity. Only people who have a direct interest in the trust, such as beneficiaries or potential heirs, usually have the right to challenge it.

The process often involves reviewing the trust’s terms, financial records, and the circumstances under which it was created. If you wish to start a dispute, you must follow specific legal steps and meet strict timelines.

Legal challenges can be complex. They may include allegations that the trustee is not acting in the best interests of the beneficiaries or is mismanaging the assets. For a detailed explanation of who can contest a trust and under what conditions, review the legal guidelines for contesting a trust in BC.

Court Intervention

If disputes cannot be settled privately, you may need to ask a court to resolve the matter. Courts in British Columbia handle trust disputes if there is evidence of trustee misconduct, unclear trust terms, or disagreements between beneficiaries and trustees.

The court can:

Remove or replace a trustee

Interpret or enforce trust terms

Require financial accounting by the trustee

Order the trustee to take or stop specific actions

Sometimes, before going to court, parties use alternative dispute resolution methods like mediation. This can help resolve issues faster and with less expense than a full court case.

Comparison to Other Trust Structures

Life interest trusts work differently from other trust types like bare trusts and discretionary trusts. Key distinctions lie in control, distribution, and the rights of beneficiaries.

Differences from Bare Trusts

A bare trust is a simple arrangement where the beneficiary has full rights to the trust property and the trustee holds legal title only. In a bare trust, you as the beneficiary can demand the property be transferred into your name at any time.

In contrast, a life interest trust allows one or more people, such as you or your spouse, to benefit from income or use of the property during their lifetime, but the capital is held for others after their death. Bare trusts do not have this life interest structure.

Taxation is another key difference. With a bare trust, the income and capital gains are reported directly by the beneficiary. A life interest trust usually pays taxes at the highest marginal rate unless certain rules apply. Life interest trusts are also subject to rules such as the 21-year deemed disposition in British Columbia, which does not apply to bare trusts.

Differences from Discretionary Trusts

A discretionary trust gives the trustee the power to decide which beneficiaries receive income or capital and in what amounts. With this structure, you might be named as a beneficiary, but you have no fixed right to income or assets.

A life interest trust, however, gives a specific person (often the settlor or their spouse) the right to all income from the trust during their life. After that person's death, the capital passes to other named beneficiaries. The trustee’s powers are more limited in a life interest trust because they must respect the life tenant’s rights.

Discretionary trusts are commonly used for estate planning flexibility, especially where beneficiaries’ needs may vary. In a life interest trust, allocations are set out clearly. In British Columbia, life interest trusts can be a key way to provide for a surviving spouse while preserving the capital for children or charities.

Considerations for Estate Planning

When planning your estate in British Columbia, it is important to think about how a life interest trust fits into your overall strategy. These trusts can help you control the use of assets during a beneficiary's lifetime.

Benefits of Life Interest Trusts:

Provide financial security to a loved one, such as a spouse or partner

Protect assets for future generations

Manage property in case of incapacity

You must also consider the legal requirements. Proper documents must be prepared and signed according to British Columbia law. If you do not have a will, your assets will be split based on provincial rules, not your wishes.

Tax implications are another key point. Life interest trusts can impact taxes for both the estate and beneficiaries. It is often helpful to seek advice from professionals who understand trust and estate planning in BC.

You may want to list your goals before you start—such as protecting minor children, reducing taxes, or ensuring privacy. Discuss your estate plan with your family to avoid misunderstandings and disputes later.

Always review your plan if your family or financial situation changes. This helps keep your estate plan up to date and effective.

Recent Developments Affecting Life Interest Trusts

You should be aware of new rules that affect life interest trusts in British Columbia. Changes in tax regulations may have an impact on how you plan your estate. These changes can also affect how trust assets are treated.

A major development is the 21-year deemed disposition rule. Every 21 years, a trust is seen as selling its assets at fair market value. This rule means that your trust may face tax on capital gains, even if the assets have not actually been sold.

When a beneficiary of a life interest trust dies, new rules require the trust to recognize any capital gains. The trust is then deemed to dispose of its assets at fair market value. This can result in immediate tax consequences for your trust.

It is important to note these changes because they affect your tax obligations and estate planning strategies.

Key points to keep in mind:

Trust assets may be taxed even if not sold.

Capital gains are triggered by the 21-year rule or the death of a beneficiary.

Trust planning now requires more care and review to avoid unexpected taxes.

The Final Verdict

Life interest trusts offer an effective way to balance the needs of current and future beneficiaries, making them especially useful in complex family or financial situations. Careful planning and legal precision are essential to ensure the trust functions as intended and complies with BC law.

For advice on whether a life interest trust is right for your estate plan and assistance with setting one up, contact the lawyers at Parr Business Law. Our team is here to help you protect your assets and provide for your loved ones with clarity and confidence.