Tax Implications of Passing a Business to Your Children in BC: Key Legal and Financial Considerations

Passing a business to your children can be a meaningful way to preserve a family legacy, but it also involves complex tax and legal considerations. In British Columbia, business succession may trigger capital gains, affect eligibility for tax exemptions, and require careful planning to minimize tax exposure. Without proper structuring, the financial burden on the next generation can be significant.

This article outlines the key tax implications and legal considerations involved in transferring a business to your children in BC, helping you plan for a smooth and tax-efficient transition.

Overview of Business Succession in BC

Passing a business to your children in British Columbia requires careful legal planning, clear eligibility steps, and close attention to tax and corporate rules. You must align your succession plan with provincial law and federal tax legislation to avoid costly mistakes.

Legal Framework for Succession

You must follow both corporate law and estate law when transferring your business.

If you operate through a corporation, the Business Corporations Act (BC) governs how you transfer shares. You need to review your articles, shareholder agreements, and any share restrictions before making changes. Some agreements limit who can own shares or require approval from other shareholders.

Your estate plan also affects the transfer. A will can direct who receives your shares, but probate and tax rules still apply. Many business owners use tools to coordinate wills, trusts, and corporate documents.

Federal tax law also applies. The Income Tax Act may treat a transfer as a sale at fair market value, even if you gift the shares. This rule can trigger capital gains tax.

Eligibility for Business Transfer

You must confirm that your child is legally able to receive and hold ownership.

In most cases, your child can inherit or receive shares in a BC corporation. However, corporate records must reflect the transfer properly. The company must update its central securities register and issue new share certificates if required.

If your child is a minor, you cannot transfer control directly without a trustee. You may need to create a trust to hold shares until your child reaches the age of majority.

You should also review:

Shareholder agreements

Buy-sell clauses

Restrictions on foreign ownership

Financing agreements with lenders

Lenders may require consent before ownership changes. Ignoring these steps can breach your contracts.

Key Considerations When Passing a Business

You need a structured succession plan that addresses tax, control, and timing.

A clear succession plan identifies who will manage the business and how ownership will shift. The Province outlines the basics of business succession planning in BC. Planning early reduces conflict and limits disruption.

Tax planning plays a central role. You may qualify for the Lifetime Capital Gains Exemption if your corporation meets the requirements for qualified small business corporation shares. If structured properly, an estate freeze can cap your tax liability and allow future growth to pass to your children.

You should also consider:

Whether your child is active in the business

How you will treat other children fairly

Your retirement income needs

The risk of reassessment by the Canada Revenue Agency

Each decision affects your tax exposure and the long-term stability of your business.

Tax Consequences of Transferring a Business to Children

When you transfer your business to your children in British Columbia, the Income Tax Act can trigger immediate tax consequences. You must plan for capital gains, attribution rules, and the proper use of available exemptions.

Deemed Disposition and Capital Gains

When you transfer shares of your corporation to your child, the Canada Revenue Agency may treat the transfer as a deemed disposition. This means you are considered to have sold the shares at fair market value, even if you gift them or sell them at a low price.

If the shares increased in value, you will realize a capital gain. You must report 50% of that gain as taxable income. This can create a large tax bill in the year of transfer.

Recent changes under intergenerational business transfer rules allow certain share transfers to children to receive capital gains treatment instead of being taxed as dividends. You must meet strict conditions, including share ownership requirements and timelines for transferring control.

If you fail to meet these rules, the CRA may recharacterize the transaction. This can result in higher tax and possible penalties.

Attribution Rules

Attribution rules can apply if you transfer property to your child for less than fair market value. These rules aim to prevent income splitting within families.

If your child is a minor, income from the transferred property may be taxed in your hands. This includes dividends from corporate shares. Capital gains are generally not attributed back to you, but other income can be.

You must also consider section 84.1 of the Income Tax Act. In some cases, selling shares to a corporation owned by your child can trigger a deemed dividend instead of a capital gain. This rule has created challenges in the past, which led to changes under Bill C-208.

You can review key updates in new tax laws on transferring a family business. These rules require proper documentation and proof that your child will take over the business.

Lifetime Capital Gains Exemption

You may be able to reduce or eliminate tax using theLifetime Capital Gains Exemption (LCGE). This exemption applies to qualified small business corporation shares.

To qualify, your corporation must meet asset tests. At least 90% of the company’s assets must be used in an active business in Canada at the time of sale. Additional holding period tests also apply.

If you qualify, you can shelter up to your available exemption limit against capital gains. This can significantly reduce the tax owed on a transfer to your child.

Structuring the Transfer for Tax Efficiency

You can reduce tax costs and protect your lifetime capital gains exemption by choosing the right legal structure. Careful planning helps you shift future growth to your children while staying within federal tax rules.

Estate Freeze Strategies

An estate freeze lets you lock in the current value of your business for tax purposes. You exchange your common shares for fixed‑value preferred shares, and your children subscribe for new common shares.

This structure moves future growth to your children. Your preferred shares keep today’s value, which limits the capital gain that may arise on your death.

You often use this approach as part of broader tax planning for succession and business transition. It works best when your company expects steady growth.

You must complete a proper valuation. The Canada Revenue Agency may challenge the freeze if the value does not reflect fair market value.

You should also review:

Access to your lifetime capital gains exemption (LCGE)

Control rights attached to preferred shares

A shareholder agreement that protects your position

A freeze can defer tax, but it does not remove it. Your estate may still face tax on the fixed-value shares later.

Use of Family Trusts

A family trust can hold shares for your children instead of transferring them directly. This structure gives you flexibility and control.

You appoint trustees, often including yourself. The trustees decide when and how to distribute income or shares to beneficiaries.

A trust can help with income splitting and long‑term planning. It also supports structured ownership under the updated 2024 intergenerational business transfer rules in Canada.

Key benefits include:

Creditor protection for beneficiaries

Control over young or inactive children

Flexibility to allocate capital gains

You must follow attribution and trust reporting rules. Trusts now face enhanced annual reporting requirements, and errors can lead to penalties.

A trust works best when you want gradual transition and ongoing oversight.

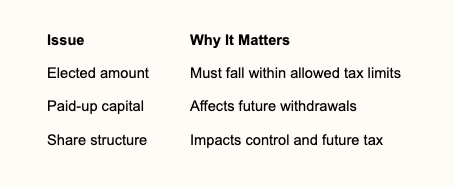

Rollovers Under Section 85

Section 85 of the Income Tax Act allows you to transfer shares to a corporation on a tax‑deferred basis. You and the corporation file a joint election to choose the transfer value.

This process avoids triggering an immediate capital gain. Instead, you defer tax until a later sale.

You often use this rollover in combination with an estate freeze or holding company structure. Many advisers discuss this in guides on transferring your business to the next generation in Canada.

Important factors include:

You must prepare the election forms accurately and file them on time. Late or incorrect filings can remove the tax deferral and create immediate tax liability.

GST and PST Implications

When you transfer a business to your children in British Columbia, you must address both federal GST and provincial PST rules. The tax result depends on whether you transfer shares or assets and whether you meet specific election or exemption rules.

Taxable Supplies and Exemptions

If you sell business assets, GST may apply to taxable supplies such as equipment, inventory, and certain intangible property. However, you may jointly elect with your child to treat the transfer as a sale of a business or part of a business so that no GST is payable at closing. The Canada Revenue Agency explains this election in its guidance on tax implications of selling a business.

For PST, British Columbia generally charges 7% on taxable goods and certain software unless an exemption applies. The province outlines how PST applies in a bulk sale in its guidance on buying and selling a business in BC.

Key differences often depend on structure:

Share sale: GST and PST usually do not apply to the shares themselves.

Asset sale: GST may apply unless you file a joint election; PST may apply to taxable goods.

You should review each asset class before finalizing the transfer.

Registration Requirements

If your child continues operating the business, they must consider GST and PST registration. A person who carries on a commercial activity and exceeds the small supplier threshold must register for GST and charge 5% on taxable supplies.

For PST, registration depends on whether the business sells taxable goods or services in BC. The province explains PST registration duties in its small business guide to PST.

You must also address clearance certificates. In BC, a purchaser should obtain a PST clearance certificate before completing a bulk transaction. Without it, your child may become liable for unpaid PST.

Take these steps before closing:

Confirm GST registration status.

Confirm PST registration and filing history.

Obtain required clearance certificates.

Proper registration and documentation reduce the risk of unexpected tax assessments after the transfer.

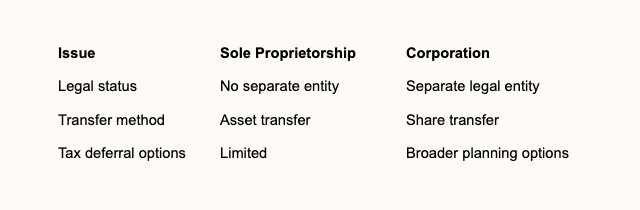

Corporate Versus Sole Proprietorship Transfers

The tax treatment and legal structure of your business will affect how you transfer it to your children. You must consider how income is taxed, how assets move, and who carries legal responsibility after the transfer.

Taxation Differences

If you operate as a sole proprietorship, you and the business are the same legal entity. When you transfer assets to your child, you may trigger a taxable disposition at fair market value.

The Canada Revenue Agency requires you to report any capital gain on business assets, including goodwill. You may defer tax in limited cases, but you do not have access to corporate rollover rules that apply to incorporated businesses.

In contrast, if you own shares in a corporation, you can transfer those shares to your child. You may use tools such as a Section 85 rollover for transferring assets to a corporation to defer immediate tax when restructuring before the transfer.

A corporation also allows you to plan around share value and retained earnings. You may qualify for the Lifetime Capital Gains Exemption if the shares meet the requirements for qualified small business corporation shares.

The table below outlines key differences:

Ownership and Liability Considerations

In a sole proprietorship, you remain personally liable for all debts and obligations. When you transfer the business, your child must take over assets and may need to assume liabilities directly.

Creditors may still pursue you for past obligations. This risk does not end simply because you pass control to your child.

A corporation provides limited liability. The company, not you personally, owns the assets and owes the debts.

When you transfer shares, you transfer ownership without changing the legal identity of the business. Contracts, leases, and licences usually remain in the corporation’s name, which can make the transition more stable.

If you are considering incorporation before a transfer, review the tax and legal steps involved in transitioning from sole proprietorship to corporation.

Impact of Share versus Asset Sales

When you transfer a business to your children in British Columbia, you must decide whether to sell shares or sell assets. This choice affects how much tax you pay, when you pay it, and whether you can use valuable tax relief.

Taxation of Asset Sales

In an asset sale, your corporation sells its individual assets, such as equipment, inventory, and goodwill. The corporation pays tax on any gains.

You may face two levels of tax. First, the corporation pays corporate income tax on capital gains and recaptured depreciation. If you later withdraw the sale proceeds as dividends, you pay personal tax on those amounts.

Certain assets create specific tax results:

Depreciable property may trigger recapture of capital cost allowance (CCA), which is fully taxable as business income.

Capital property may result in a capital gain, with 50% of the gain taxable.

Inventory is taxed as regular business income.

Asset sales can increase the total tax cost.

You should also consider that sale proceeds remain in the corporation. You must plan carefully before removing funds for personal use.

Taxation of Share Sales

In a share sale, you sell your shares of the corporation directly to your children. The corporation itself does not sell its assets.

You report a capital gain on the sale of your shares. Only 50% of that gain is taxable.

If your company qualifies as a small business corporation, you may claim the Lifetime Capital Gains Exemption (LCGE). This exemption can shelter a significant portion of the gain from tax. Guidance on the tax impact of a share sale appears in discussions of asset vs share sale tax implications.

A share sale often results in a single level of tax at the personal level. However, your children inherit the corporation with its existing liabilities. You should review legal and financial risks before choosing this structure.

Intergenerational Business Transfer Rules

Federal tax law sets strict conditions when you transfer shares of your corporation to your child. If you meet these rules, you can report a capital gain instead of a dividend and may claim the lifetime capital gains exemption.

Qualifying for Intergenerational Transfers

Section 84.1 of the Income Tax Act can turn your sale into a deemed dividend if you sell shares to a corporation your child controls. This often leads to higher tax than a sale to an arm’s-length buyer.

The intergenerational business transfer (IBT) rules allow capital gains treatment if you meet specific conditions. The business must qualify as a small business corporation, family farm corporation, or family fishing corporation.

You must transfer shares to a corporation controlled by your adult child or grandchild. The child must have real control and involvement in the business after the transfer.

Under updated rules, you must also meet timelines for transferring management and ownership. If you fail to meet these tests, the CRA can reassess the transaction as a dividend.

Keep clear records of share ownership, voting control, and your child’s role in daily operations. These details matter during a CRA review.

Recent Federal Legislative Changes

Parliament first addressed these issues through Bill C-208. Later amendments tightened the rules to limit access to genuine family successions.

Changes effective January 1, 2024 added stricter conditions. You must now choose between two transfer paths: an immediate transfer or a gradual transfer.

Under the immediate option, your child must gain legal and factual control within a short period. Under the gradual option, you have a longer transition period, but you must reduce your involvement and economic interest over time.

The law also requires your child to retain control of the corporation for a minimum period. If your child disposes of the shares too soon, the CRA may reverse the tax treatment.

These amendments aim to treat family transfers more like third-party sales, but only when you complete a real and lasting succession.

Compliance and Reporting Obligations

When you transfer your business to your children, you must meet specific filing and disclosure rules under the Income Tax Act. These rules apply whether you use an immediate sale or a gradual transfer structure.

You need to report the share sale on your personal or corporate tax return. You may also need to file elections or supporting documents to confirm that the transfer qualifies as an intergenerational business transfer under the updated rules.

Key compliance steps may include:

Reporting capital gains or claiming the lifetime capital gains exemption

Filing any required elections within the prescribed deadline

Maintaining documents that show your child has acquired control of the business

Keeping valuation reports to support the fair market value of the shares

You must also consider Canada’s expanded mandatory disclosure rules. Certain transactions that meet defined risk criteria may trigger reporting obligations, as outlined in the CRA’s guidance on mandatory disclosure rules in Canada.

Failure to file required forms on time can result in penalties and extended reassessment periods.

You should retain corporate records, shareholder agreements, and financing documents for audit purposes. Clear documentation helps demonstrate that the transfer reflects a genuine succession plan rather than a tax avoidance arrangement.

Minimizing Tax Liabilities

You can reduce taxes when transferring your business by structuring the deal correctly and choosing the right time. Careful planning helps you preserve access to key tax rules and avoid costly mistakes.

Planning with Professional Advisors

You face complex federal tax rules when passing a business to your children in British Columbia. Capital gains tax, shareholder benefit rules, and anti‑avoidance provisions can apply at the same time.

You should work with a tax accountant and a tax lawyer who understand the updated rules for intergenerational transfers. Budget changes have revised how Canada treats family share sales, especially after new rules for transferring a family business to the next generation.

Professional advisors can help you:

Confirm that your corporation qualifies as a Qualified Small Business Corporation (QSBC)

Structure the sale to allow you to claim the Lifetime Capital Gains Exemption (LCGE)

Use tools such as an estate freeze or a Section 85 rollover when appropriate

An estate freeze can shift future growth to your children while you keep control through preferred shares. A Section 85 rollover may allow you to defer tax when transferring assets into a corporation. You must follow strict rules to avoid having the Canada Revenue Agency reclassify the transaction.

Timing of Transfer

The timing of your transfer can change the amount of tax you pay. You should review your company’s retained earnings, asset mix, and share structure before setting a date.

If your shares qualify for the LCGE, you may reduce or eliminate capital gains tax on a portion of the gain. However, your corporation must meet asset tests at the time of sale and during the prior 24 months.

You should also consider whether to transfer the business gradually. Some families use multi‑year plans. A phased transfer can allow you to spread capital gains across tax years and manage cash flow.

You must also align the transfer date with your personal retirement income plan. A poorly timed sale can push you into a higher tax bracket and increase your overall tax burden.

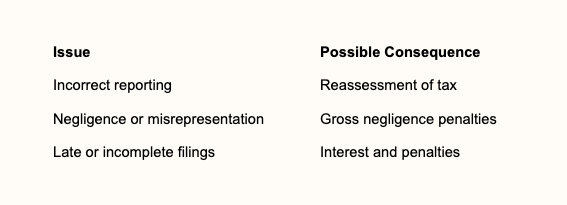

Potential Penalties and Audits

When you transfer a business to your children, the Canada Revenue Agency (CRA) may review the transaction. You must meet all conditions under the Income Tax Act, including the updated rules for intergenerational transfers. If you fail to comply, the CRA can reassess the sale.

You face risk if the transfer does not meet the requirements set out in tax changes to intergenerational business transfers in Canada. For example, the CRA may deny capital gains treatment and instead treat the proceeds as a taxable dividend. This can increase the tax you owe.

Common audit triggers include:

Unreasonable share valuations

Lack of proper documentation

Failure to transfer legal and factual control

Non-compliance with holding period rules

If the CRA finds errors, you may face:

Interest applies daily on unpaid tax. Penalties can increase if the CRA determines that you made false statements knowingly or with carelessness.

You should keep detailed records of the sale agreement, valuation reports, and corporate resolutions. Clear documentation helps support your position if the CRA reviews your file.

Post-Transfer Tax Planning

After you transfer the business, you must review your new tax position. Your income may shift from business profits to salary, dividends, or loan repayments. Each type of income carries different tax rules.

You should confirm that the transfer met the conditions under the updated rules for intergenerational business transfers. If the Canada Revenue Agency finds that the conditions were not met, it may reassess the transaction.

Consider these ongoing tax areas:

Share structure and dividends: Review who holds voting and non-voting shares. Plan dividend payments to manage personal tax.

Capital gains exemption: Ensure the company continues to meet the tests for Qualified Small Business Corporation shares, if relevant.

Estate planning updates: Align your will and powers of attorney with the new ownership structure.

Corporate compliance: File corporate tax returns and information slips on time.

You may also need to monitor repayment terms if your children issued a promissory note for the purchase. Interest must be reasonable and properly reported.

If you completed an estate freeze or used a trust, maintain proper records. Trust reporting rules are strict, and errors can lead to penalties.

Early and regular reviews reduce risk. Many advisors stress the importance of starting early. Regular meetings with your tax advisor help ensure the structure remains compliant and tax efficient.

Provincial-Specific Tax Considerations in British Columbia

When you transfer a business to your children in British Columbia, you must review both provincial and federal tax rules. The province follows federal rules for income tax, but it also applies its own rates and credits.

British Columbia’s 2026 budget introduced targeted tax measures and updated its fiscal outlook. You can review the government’s summary of the B.C. Provincial budget tax changes to confirm current rules that may affect your planning.

You should also monitor broader updates from the British Columbia 2026 provincial budget. Changes to business incentives or tax credits can affect the timing and structure of your transfer.

Key provincial factors to review include:

B.C. personal income tax rates that apply if you trigger capital gains on a share sale

Corporate income tax rules if your company remains active after the transfer

Provincial tax credits or incentives that may change after ownership shifts

Speculation and vacancy tax, if your business holds residential property

British Columbia does not charge a provincial estate tax. However, you may still face capital gains tax on deemed dispositions at death.

You should confirm current provincial rates and thresholds before you finalize any transfer. Small changes in tax policy can affect your after-tax outcome and your children’s future tax position.

Family and Legal Considerations

When you pass your business to your children, you must address more than tax rules. You also need to manage family expectations, control issues, and legal structure.

Clear communication reduces conflict. You should explain your plan early and document your decisions in writing.

Key family issues to consider:

Will all children receive ownership, or only those active in the business?

How will you treat children who are not involved?

Who will control daily operations after the transfer?

What happens if a child wants to exit the business?

Unequal treatment can create tension. You may need to balance business shares with other estate assets.

Legal structure also matters. You must ensure your corporation meets the rules for intergenerational transfers. For example, updated federal rules affect how you transfer shares to children under new tax laws for family business transfers.

You should also review shareholder agreements. These agreements set rules for voting rights, share sales, and dispute resolution.

Professional advice is essential. Engaging tax and legal advisors helps you comply with evolving rules, including recent changes to intergenerational share transfer rules in Canada.

Finally, update your will and estate plan. Your business succession plan should align with your broader estate goals to avoid unintended tax or legal issues.

The Final Verdict

Transferring a business to your children in BC requires careful planning to manage tax liabilities and ensure the long-term viability of the business. Strategic use of exemptions, trusts, and succession planning tools can help reduce taxes and avoid unintended consequences.

For tailored advice on business succession and tax planning, contact the attorneys at Parr Business Law. Our experienced team can help you structure a plan that protects your business, your family, and your financial legacy.