Why Business Owners in BC Shouldn’t DIY Their Wills: Legal and Financial Risks to Consider

Running a business in British Columbia demands careful planning. Your will controls what happens to your company, your shares, and your personal assets after you pass away. If you own a business in BC, you should not draft your own will because even small legal errors can put your company, your family, and your estate at risk.

BC law sets strict rules for signing and witnessing a valid will. A DIY document may not deal properly with corporate shares, business succession, or probate fees. Mistakes such as improper signing or unclear terms can lead to court disputes and added costs.

As a business owner, you face added issues such as succession planning, tax impact, and privacy. Some estates may benefit from tools like a corporate will to manage probate fees. Proper legal advice helps protect your business continuity and ensures your estate plan reflects your goals.

Legal Complexities of Will Preparation in BC

British Columbia sets strict legal rules for creating a valid Will. As a business owner, you must follow these rules closely or your estate plan may fail.

Provincial Laws Governing Wills

In British Columbia, the Wills, Estates and Succession Act (WESA) governs how you create, sign, and interpret a Will. You must meet formal signing and witnessing rules unless a court later validates the document.

You can review key requirements under the Wills, Estates and Succession Act BC rules and insights. These rules affect how gifts are distributed, how executors act, and how family members can challenge your estate.

If you own a private company, your Will must also address:

Transfer of corporate shares

Shareholder agreements

Buy-sell terms

Director and voting control

General guidance from the Province outlines the broader legal framework in Wills and estate planning in British Columbia.

When you draft your own Will without legal advice, you may overlook how corporate law, tax law, and estate law interact. That risk increases if you hold assets through a holding company or trust.

Risks of Invalid Documents

A Will becomes invalid if you fail to meet legal formalities. Common mistakes include improper witnessing, unclear signatures, and missing pages.

If your Will is invalid, the court may treat you as though you died without one. Your estate would then follow intestacy rules under WESA, not your personal wishes.

Business assets create added risk. For example:

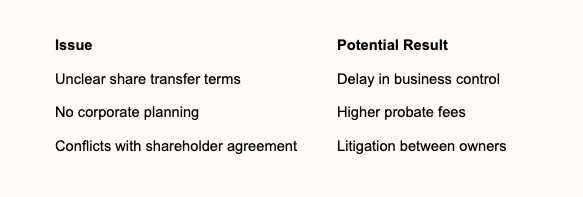

Some business owners use multiple Wills to reduce probate fees on private company shares. If you structure this improperly, you can create confusion or invalidate part of your plan.

Errors in drafting often lead to estate disputes. Litigation can freeze business operations and strain family relationships.

Testator Capacity Requirements

You must have legal capacity when you sign your Will. This means you understand:

The nature of making a Will

The extent of your property

The people who may expect to benefit

Capacity issues often arise when illness, age, or cognitive decline affects decision-making. If someone challenges your capacity, the court will examine medical records and witness evidence.

Business ownership adds complexity. You must understand the value and structure of your company, including share classes and liabilities.

If a court finds that you lacked capacity, it can declare your Will invalid. Your estate may then pass under a prior Will or under intestacy rules.

As a business owner, you face higher stakes because your company’s continuity may depend on the validity of your Will.

Common Pitfalls of Do-It-Yourself Wills

When you draft your own will, small errors can create serious legal and financial problems. Business owners face added risks because their estates often include corporations, shareholders, and ongoing contracts.

Ambiguous Clauses

Vague language often leads to disputes.

If you write that your shares go to “my children” without naming them, you create room for conflict. Blended families, stepchildren, and estranged relatives can challenge what you meant. Courts may need to interpret your wording, which increases delay and cost.

Template forms also fail to adjust to British Columbia law. Unclear or poorly drafted clauses can expose your estate to challenges.

Business assets raise additional issues. You may need to address voting control, shareholder agreements, or buy-sell terms. If your will does not align with these documents, your executor may face legal barriers when trying to transfer ownership.

Clear drafting matters when your company supports employees, partners, and your family’s income.

Omitted Beneficiaries

Leaving someone out by mistake can trigger a legal claim.

In British Columbia, certain family members can challenge a will if you do not make adequate provision for them. If you forget to name a child or fail to consider a new spouse, the court may review your estate plan.

Many online forms do not prompt you to review all potential beneficiaries and generic templates often miss complex family and financial situations.

Business owners must also think beyond family. You may intend to leave shares to one child active in the company and other assets to another child. If you do not structure this carefully, you risk unequal results or forced asset sales.

You need a plan that reflects both your family structure and your business reality.

Improper Signing and Witnessing

Even a well-written will fails if you do not sign and witness it properly.

British Columbia law sets strict rules for execution. You must sign in the presence of two qualified witnesses, and they must sign in your presence. If you select a beneficiary as a witness, you may void that gift.

Errors in signing and witnessing rank among the most common DIY problems.

If your will does not meet legal standards, the court may treat it as invalid. Your estate could then pass under intestacy rules, not according to your wishes.

For a business owner, that outcome can disrupt operations, freeze decision-making, and harm the value of your company.

Potential Financial Consequences for Business Owners

A poorly drafted will can create tax problems and disrupt the transfer of your company. These issues often lead to higher costs, court disputes, and loss of control over how your business continues after your death.

Unintended Tax Liabilities

When you own shares in a private company, your death can trigger a deemed disposition under Canadian tax law. The Canada Revenue Agency treats your assets as if you sold them at fair market value.

If your will does not plan for this, your estate may face a large capital gains tax bill. Your executor may need to sell business assets or shares to pay the tax.

This problem often arises when owners try to pass the business directly to children without proper planning tools. Strategies such as an estate freeze, family trust, or Section 85 rollover require careful legal and tax advice. A general online will form will not address these steps.

Tax exposure can affect both your company and your family. Without proper structure, your estate may lose access to valuable tax deferrals or exemptions.

Even small drafting errors can cost tens of thousands of dollars. You remain responsible for the results, even if you used a low‑cost template.

Business Succession Failures

Your will must work with your shareholder agreements, corporate documents, and succession plan. If these documents conflict, disputes can follow.

For example, your will may leave shares to a family member who does not work in the business. A shareholder agreement may require those shares to be offered to other owners first. This conflict can lead to litigation or a forced sale.

Effective business succession and estate planning in British Columbia addresses voting control, management authority, and funding for buyouts. A do‑it‑yourself will rarely coordinate these details.

You should also consider:

Who will manage daily operations

How debts and personal guarantees will be handled

Whether key employees will remain

If you do not set clear terms, your executor may struggle to run the company. Revenue can drop quickly during uncertainty. In some cases, the business fails before the estate resolves ownership issues.

Impact on Business Continuity

When you draft your own will, you risk delays, confusion, and loss of control over your company. Poor planning can interrupt daily operations and trigger costly disputes that affect staff, clients, and revenue.

Disruption of Operations

If your will does not clearly name who will control your shares or act as executor, your business can stall. Banks may freeze accounts. Key contracts may sit unsigned.

You may also fail to align your will with your shareholder agreement. This mismatch can block ownership transfers or voting rights. In some cases, surviving partners cannot make urgent decisions without court approval.

A weak estate plan can also disrupt existing continuity planning. Government guidance on preparing your business for disasters and emergencies stresses the need for clear roles and decision-making authority. Your will forms part of that structure.

If you leave gaps, your staff may not know who leads the company. Suppliers may tighten terms. Clients may question stability. Even short delays can affect cash flow and long-term contracts.

Legal Disputes Among Heirs

If you divide business assets without clear instructions, you may create conflict among your heirs. One child may inherit shares while another expects management control. Disputes often follow.

Without a detailed plan, beneficiaries may argue over valuation, dividends, or sale terms. These conflicts can lead to court applications that tie up company assets for months.

A proper continuity framework identifies risks and protects operations during a crisis. Business continuity planning defines roles, safeguards, and recovery steps, as explained in Understanding Business Continuity Plans. Your will should support that structure, not weaken it.

When heirs fight over ownership, employees notice. Key staff may leave due to uncertainty. Lenders and investors may reassess their risk. Clear legal drafting reduces these risks and protects both your family and your company.

Importance of Tailored Legal Advice

You face legal and financial risks when you draft your own will without advice that reflects your business structure. Proper legal guidance aligns your succession plan and asset distribution with British Columbia law and your company’s governing documents.

Customized Business Succession Planning

You cannot rely on a simple will template if you own shares in a corporation, hold partnership interests, or operate as a sole proprietor. Each structure carries different legal duties and tax effects.

A lawyer helps you create a clear plan for who will control and who will own the business. These are not always the same people. Control may pass to a director or manager, while ownership may transfer to family members or a trust.

Under business succession planning in British Columbia, you must consider shareholder agreements, buy-sell clauses, and restrictions on share transfers. If your will conflicts with these documents, the agreement usually prevails.

You also need to plan for incapacity, not just death. A properly drafted power of attorney and corporate documents allow someone you trust to manage operations and banking without court delays.

Without tailored advice, you risk disputes between family members, business partners, and key employees.

Ensuring Proper Asset Distribution

Your business assets may not pass the way you expect. Shares, retained earnings, real estate, and intellectual property require precise language in your will.

A lawyer ensures your will complies with the Wills, Estates and Succession Act in British Columbia. This law allows certain family members to challenge a will if they believe it does not make adequate provision for them.

You must also address tax consequences. The Canada Revenue Agency may treat your death as a deemed disposition of shares, which can trigger capital gains tax. Poor planning can force your executor to sell business assets to pay taxes.

Clear drafting reduces ambiguity. Your will should:

Identify specific business interests

State how debts and taxes will be paid

Coordinate with trusts, holding companies, or insurance policies

When you receive tailored legal advice, you reduce the risk of litigation and protect both your family and your business operations.

Privacy and Confidentiality Concerns

When you draft your own will, you may expose sensitive business and personal information. A will often includes details about assets, shareholders, debts, and family members.

If you store drafts on a personal device or online platform, you must consider your legal duties around privacy. In British Columbia, private sector organizations must follow the Personal Information Protection Act (PIPA). This law governs how you collect, use, and disclose personal information.

Your will may contain:

Employee information

Client names or financial details

Shareholder agreements

Banking and investment records

If you handle this information without proper safeguards, you risk unauthorized access or disclosure. Legal issues from privacy breaches can be serious and disruptive.

Confidential business information also requires protection. Policies and safeguards help prevent misuse and reduce legal risk.

A lawyer helps you manage these risks. You receive advice on secure storage, limited disclosure, and proper documentation. This approach supports both your estate plan and your legal obligations as a business owner.

Role of Professional Estate Planners in BC

Professional estate planners in British Columbia address both your business structure and your family situation. They align corporate documents, tax planning, and your will to reduce conflict and costly errors.

Expertise in Corporate and Family Law

When you own a business, your estate plan must reflect your corporate structure. A planner reviews your shareholder agreements, articles, and any existing trusts to ensure they match your will.

Many business owners do not realize that personal and corporate documents must work together. If they conflict, your plan can fail at a critical time.

You also need to account for succession, tax exposure, and asset protection. Professional advisors often coordinate succession plans and trusts as part of broader corporate legal advice in estate planning.

They also consider family law risks. Divorce, blended families, and unequal distributions can affect business control. You reduce uncertainty when your estate plan reflects both corporate and family realities.

Mitigating Litigation Risks

A DIY will often fails to address what happens to your shares or voting rights. This gap can lead to disputes among family members, co-owners, or key employees.

In British Columbia, if you die without a valid will, the Wills, Estates and Succession Act governs distribution. This can create uncertainty for your company.

Professional planners reduce this risk by:

Clarifying who inherits shares

Setting out buy-sell terms

Coordinating insurance funding

Naming appropriate executors

They also document your intentions clearly. Precise drafting lowers the chance of wills variation claims or disputes over business control, which helps protect both your estate and your ongoing operations.

Cost Comparison: DIY vs Professional Will Preparation

The price gap between a DIY will and a professionally drafted will can appear large at first glance. However, you must look beyond the upfront fee and consider legal risk, court costs, and the impact on your business.

Hidden Expenses of DIY Wills

A basic online will in British Columbia can cost about $40, while a lawyer-prepared will may range from $2,000 to $4,000 depending on complexity. The lower price can seem attractive, especially if you want to reduce expenses.

However, business ownership adds legal layers that templates often fail to address. Share structures, shareholder agreements, and corporate assets require precise language. If your will creates confusion, your executor may need court direction.

Legal disputes can erase any savings. Some cases involving unclear estate plans have led to more than $100,000 in legal fees and business losses. Litigation also delays asset transfers and disrupts operations.

You must also consider probate delays, accounting costs, and tax advice needed to fix drafting errors. These expenses often exceed the original legal fee you tried to avoid.

Long-Term Financial Security

A professionally drafted will support business continuity. Your lawyer can coordinate your will with corporate documents, tax planning, and succession terms. This reduces the chance of conflict among partners or family members.

DIY wills often fail because of missing formalities or unclear instructions. Courts may apply intestacy rules if your document is invalid, which increases administrative costs and removes your control over distribution. The Province of British Columbia explains how estates are handled under law in its overview of wills and estate planning.

When you own a business, your estate may include:

Corporate shares

Retained earnings

Commercial property

Ongoing contracts

Each item carries tax and legal consequences. Professional planning helps protect your company’s value, reduce tax exposure, and support a smooth transfer. This approach focuses on preserving long-term financial stability rather than minimizing short-term cost.

Updating and Amending Wills for Business Owners

Your will must reflect the current structure of your company and your personal circumstances. Even small changes can affect control, tax planning, and who receives your business interest.

Changing Corporate Structures

When you change your corporate structure, you must review your will right away. This includes incorporation, adding shareholders, creating a holding company, or reorganizing shares.

Your will should clearly state what type of shares you own and who will receive them. If you complete an estate freeze or issue new classes of shares, your old will may no longer match your ownership.

Business interests often require coordination between your will and shareholder agreements. Business arrangements frequently need alignment between the will and corporate documents.

You should also review buy-sell terms, insurance funding, and voting control. If your will conflicts with a shareholder agreement, the agreement may limit what your executor can do. This can delay administration and create disputes among partners or family members.

Responding to Personal Life Changes

Personal events can directly affect your business succession plan. Marriage, separation, divorce, or the birth of a child may change who has legal rights to your estate.

British Columbia’s estate laws can impact how your will operates. The province’s Wills, Estates and Succession Act and probate rules set out how wills are treated after certain life events.

If you separate from a spouse but do not update your will, parts of it may fail or be interpreted differently than you expect. This can affect control of your company and voting rights tied to your shares.

You should also review guardianship plans, trusts for minor children, and the choice of executor. Your executor must understand both estate administration and business operations. Without updates, your will may not protect your company or your family as intended.

The Final Verdict

DIY wills can expose business owners in BC to significant legal and financial risks, particularly when business assets, succession plans, and tax considerations are involved. A properly drafted will ensures your business interests are protected and transferred according to your intentions.

To avoid costly mistakes and safeguard your business legacy, contact the attorneys at Parr Business Law. Our experienced team can create a comprehensive estate plan tailored to the unique needs of business owners.