Will Planning for Assets Outside of BC: Important Considerations for Effective Estate Management

When planning your will, owning assets outside of British Columbia—whether in another province or internationally—introduces added complexity to your estate.

Different jurisdictions have varying probate rules, tax laws, and legal requirements that can impact how your estate is administered. Careful planning is essential to avoid delays, reduce costs, and ensure your wishes are respected across all locations.

This article outlines important considerations for effective will planning when your estate includes assets outside of BC.

Overview of Will Planning for Assets Outside of BC

When you own property or investments outside British Columbia, preparing a will becomes more complex. Managing multiple legal frameworks and keeping clear records is essential to avoid delays and extra costs for your heirs.

Definition of Out-of-Province and International Assets

Out-of-province assets are those located elsewhere in Canada but outside of British Columbia. International assets are properties, bank accounts, investments, or business interests held in other countries.

These assets often include vacation homes, joint bank accounts, or shares in a company abroad. Holding such assets means your estate must meet different legal rules in each location. This can impact probate and taxes, sometimes causing delays or legal challenges if not addressed properly.

If these assets are not included in your will or another estate plan, they may not be distributed the way you intend. Defining your assets carefully helps prevent confusion and ensures your wishes are carried out across multiple places.

Legal Frameworks Affecting Will Planning

Different provinces and countries have their own laws for wills and estates. In Canada, each province has its rules for probating a will and distributing property. If you have assets in another Canadian province, the will may need to go through a process called resealing probate so other courts can accept it.

International assets raise even more legal issues. Some countries require a local will, while others accept a will from here. If you use just one will, it may subject all your assets to fees or taxes in the province where you died. Many people create separate wills for assets in different places to simplify administration and reduce potential legal conflicts.

It's best to consult both Canadian and foreign lawyers to ensure your estate plan fits all the local rules and avoids unwanted complications.

Importance of Comprehensive Asset Documentation

Keeping thorough and organized documentation for all assets inside and outside British Columbia is crucial. Complete records should list locations, types, and values of each asset.

A clear list helps your executor locate and manage your property quickly. It can also speed up legal processes, such as applying for probate or transferring ownership. Missing or incomplete information may result in delays, increased legal costs, or assets that remain unclaimed.

To assist your executor, update your asset records regularly. Include details like account numbers, property addresses, and contact information for any professionals managing those assets. Proper documentation can help prevent disputes among heirs and make the overall process smoother.

Jurisdictional Considerations

When planning your will for assets outside British Columbia, you must address how different regions treat property, how they may apply their own laws, and whether your wishes will be respected.

Conflict of Laws Challenges

If you own assets in more than one country or province, you may encounter conflict of laws. This means the courts in each location could apply their own rules to your property. For example, one place might demand your assets go to certain family members even if your will names others.

Resolving these conflicts can be complex. You or your estate might need to deal with legal proceedings in multiple places. In some cases, a court could ignore your BC will for property located elsewhere if their rules differ greatly from British Columbia’s laws. This is why it is essential to know how the relevant jurisdictions treat foreign wills and property distribution.

Working with legal professionals familiar with multi-jurisdictional estates can help you avoid unexpected outcomes. Careful planning can also make the probate process easier and more predictable. Find more on this issue at Parr Business Law’s discussion on multiple wills and jurisdictions.

Recognition of Foreign Wills

A key issue is whether other countries or provinces will recognize and enforce the directions in your BC will. Some jurisdictions “recognize” wills from elsewhere only if strict rules are followed. Others may have their own rules about property inheritance that overrule your wishes.

If your will does not comply with the requirements of the jurisdiction where your assets are located, it may be ignored. For example, if property law in another country says real estate must pass to your eldest child, this might override what your BC will says.

Having a separate will for each jurisdiction where you have assets can help ensure your wishes are respected. This tactic can simplify probating your estate and prevent delays or expensive legal hurdles.

Applicable Laws for Different Asset Types

The type of property you own affects which laws apply when you die. Real estate is usually governed by the laws of the country or province where it sits. For example, a home in Alberta will be dealt with under Alberta law, not BC law, even if your main will is from British Columbia.

Moveable property, like bank accounts or investments, is sometimes handled according to your main residence’s law or the law of the place where the asset is held. This can lead to confusion if the laws differ. It’s possible you will need to “reseal” your BC will in another province or country to manage these assets, or even deal with extra taxes and fees.

Wills and Estate Planning Strategies

When you own assets outside of British Columbia, a few key strategies can help you reduce legal delays, prepare for possible incapacity, and protect your estate from unexpected problems.

Use of Multiple Wills

Multiple wills are useful if you own property in more than one place. Having a separate will for each country or province where you have significant assets can make settling your estate easier. Each will is designed to meet the legal requirements of the location where your asset is held.

This approach can help speed up probate by allowing each jurisdiction to process only the assets covered by its own will. You may also lower probate fees and reduce the risk of legal conflicts if local laws change or are unclear. If you are considering this option, it is important to work with lawyers in all relevant areas so your wills do not conflict or accidentally cancel each other. Learn more about the benefits and legal issues of multiple wills for assets outside BC.

Powers of Attorney for International Assets

A power of attorney lets someone act for you if you are unable to manage your finances. If you own real estate, investments, or accounts abroad, you may need a separate power of attorney for each country. Each document must meet local legal standards to be accepted by banks or land offices.

Some places have strict rules about who can act as your attorney and how the document is prepared or witnessed. Failing to plan ahead can result in extra court steps or prevent your assets from being managed at all.

Estate Planning with Cross-Border Trusts

A cross-border trust can be used to hold and manage assets in different countries. These trusts offer privacy, can limit probate delays, and may help lower taxes in certain situations. They work well for families with children or beneficiaries living in other countries.

Setting up a cross-border trust takes careful planning to make sure it is valid and meets the tax rules of each country involved. You will need legal and tax advice from experts in each country to avoid double taxation, penalties, or unwanted legal issues. Cross-border trusts are especially suitable if you want to protect assets for minor children or support a family member with special needs in another country.

Taxation of Foreign and Out-of-Province Assets

You must address taxes in both Canada and other countries if you own property or investments outside British Columbia. Rules can be complex and often depend on where your assets are located and how they are owned. Careful planning can help avoid costly errors and penalties.

Canadian Tax Implications

If you are a resident of Canada, you are taxed on your worldwide income. This means any capital gains, interest, rent, or other income earned from assets outside BC or abroad must be included in your Canadian tax return.

Canada treats the transfer of foreign assets at death as a deemed disposition, so your estate may need to pay capital gains tax. If you hold real estate, shares, or other property outside Canada, your executor will have to calculate and report any gains as if you sold these assets right before your death.

Certain types of properties, like Canadian registered accounts, may have special rules, but most non-registered foreign assets are covered by these general rules. Professional advice is strongly recommended to accurately value and report your holdings.

Foreign Tax Obligations

Many countries tax assets, income, or gains within their borders, even if you are not a local citizen or resident. If you own property, investments, or business interests abroad, you or your estate may need to file returns and pay taxes in that country.

For example, rental income earned from a property in another country is often taxable there first. Some countries apply estate or inheritance tax on locally held assets, which could affect your heirs. Tax rules, rates, and exemptions differ widely, so you will need to check the requirements for each location where you own assets.

Failing to address local tax duties can result in penalties, delays in estate settlement, or increased costs for your beneficiaries.

Double Taxation Agreements

Double Taxation Agreements (DTAs) exist to help prevent being taxed twice on the same income. Canada has many treaties with other countries to provide relief through tax credits or exemptions.

When a DTA applies, you may be able to claim a foreign tax credit for taxes paid in the other country. This reduces your Canadian tax by the amount paid elsewhere, up to the Canadian amount owed on that income. Not all countries have DTAs with Canada, and the rules differ by agreement. If there is no treaty, it is possible to pay taxes twice on the same amount.

Determining the correct credit or exemption often requires thorough documentation and understanding of both countries' tax laws.

Reporting Requirements

Canada requires you to disclose foreign property over $100,000 in total cost on Form T1135. This is called the Foreign Income Verification Statement. It covers assets such as real estate, stocks, bonds, or bank accounts held outside Canada, but excludes personal use property like a vacation home.

Failure to file this form can lead to steep penalties even if the assets did not generate income. If you hold these foreign assets through a Canadian financial institution, there may be rules for reporting them in aggregate rather than item by item. New immigrants to Canada are usually exempt from this reporting the first year they become residents.

For more details about foreign asset reporting in Canada, see the latest government guidance.

Probate Procedures in Other Jurisdictions

When you own assets outside of British Columbia, the probate process will differ based on where those assets are located. Each region has its own laws and steps for handling wills and estates.

Probate Process for International Assets

Owning property or financial accounts in another country can require special steps after your death. Typically, a Canadian will is not automatically valid abroad. Many countries require your estate to go through their own probate process to transfer ownership of international assets.

You may need to hire a lawyer in that country to guide the process. They can help you understand local rules and ensure your estate is managed correctly. Sometimes, this may take extra time or cost more due to translation or document requirements.

In some cases, countries allow a Canadian grant of probate to be recognized if you follow specific legal steps. However, not all countries accept this.

Probate Process for Out-of-Province Assets

Generally, each province has its own rules about probate, and a grant from British Columbia is not always enough.

Some provinces in Canada allow the probate court to “reseal” an existing grant from BC. This means the will does not need to start from scratch, but there is still paperwork to complete. Other provinces may require a full probate application.

Delays are common when out-of-province probate is needed, so planning ahead can save time and money.

Ancillary Probate

Ancillary probate occurs when your main will is probated in British Columbia, but you have assets in another province or country. In this case, your executor must ask the court in the other jurisdiction to recognize the BC grant of probate before assets can be managed there.

This process is often necessary for real estate or substantial investments located outside BC. It can involve legal filings, payment of probate fees, and possibly hiring a local lawyer. Some jurisdictions make ancillary probate easier than others, especially in Canada where rules are more similar between provinces.

However, in other countries, ancillary probate may be complex or costly. Understanding these requirements ahead of time helps your executor avoid surprises and ensures your assets are distributed as you intend.

Challenges and Risks in Will Planning for Out-of-Province Assets

When your estate includes property or investments outside of British Columbia, you may face extra legal and practical problems. These issues can affect how your assets are managed, divided, and passed on.

Disputes Arising from Conflicting Jurisdictions

When assets are held in different provinces or countries, conflicts between legal systems are common. Each location may have its own rules for wills, probate, and estate taxes. Differences in these laws can create confusion or disagreement among heirs and executors.

For example, a will that is valid in British Columbia might not meet the legal requirements in another place. Certain provinces or countries may not recognize powers given to your executor. If a court in the other region refuses to accept your will, your wishes could be challenged or ignored.

This situation can lead to legal disputes or lawsuits. Your family may have to hire lawyers in several places to resolve the conflicts. To help avoid these issues, you may need to create multiple wills or get legal advice from professionals familiar with cross-border estate planning.

Delays in Asset Distribution

Managing out-of-province assets will often take much more time than dealing with assets in British Columbia. Legal systems in other provinces or countries may require extra paperwork or court approvals before your property can be transferred to beneficiaries.

If a local court does not accept documents from British Columbia, your executor might have to start a new probate process in that location. This can lead to long waits and additional expenses. Some investments or accounts may be frozen until all legal steps are complete.

Family members may have to travel or hire local lawyers to manage paperwork. As a result, loved ones could wait months or even years to receive what you have left for them.

Potential for Intestacy

If your will does not meet the legal standards where your assets are located, those items may be left out of your estate plan. In these cases, the assets can be treated as if there was no valid will. This is called intestacy.

Each province or country uses its own laws to decide who inherits in cases of intestacy. Often, the property does not go to the people you would have chosen. This can cause hardship for your intended beneficiaries and increase family disputes.

You can reduce these risks by making sure your will is valid in every region where you hold assets. Getting advice from a lawyer in the relevant area greatly decreases the chance of your estate being divided in a way you did not intend.

Role of Professional Advisors

Managing assets outside of British Columbia requires guidance from professionals who understand both local and international rules to reduce risks, avoid unnecessary fees, and make sure your estate plans reflect your wishes.

Engaging Cross-Border Legal Experts

You should work with lawyers who practise in every relevant jurisdiction. These professionals can help you prepare separate wills for each country or province. This method can make probate faster and avoid conflicts, especially if assets or beneficiaries are spread across borders. Coordinated legal advice also helps ensure that one will does not accidentally cancel another, which is a common risk in multiple will planning.

Quick tips when choosing legal advisors:

Confirm experience with international or cross-province estates

Ask how they coordinate with other lawyers

Review your documents for clarity and legal compliance

Working with Tax Professionals

Owning assets outside of British Columbia means you may face taxes on the transfer of foreign property, inheritance taxes, or double taxation if the same asset is taxed in two places.

A qualified tax advisor will understand both Canadian tax rules and those of the country where the asset is held. They can help you arrange your assets to lower taxes and prevent surprises. Common strategies include using tax treaties, gifting, naming automatic beneficiaries, or setting up trusts. This can be important for property, investments, or business interests you have abroad and may help you avoid probate fees through the use of life insurance and similar tools.

Key tax questions to ask:

Will foreign income or capital gains taxes apply to my assets?

Are there ways to avoid double taxation?

How do inheritance taxes in other countries affect my heirs?

Special Considerations for Real Property

Managing real estate outside British Columbia often requires you to prepare for legal differences and unique challenges in other locations. Each place has its own rules about property ownership, inheritance, and taxes that can affect your estate plans.

Dealing with Foreign Real Estate

When you own land or property outside BC or Canada, local laws control how that property is handled when you pass away. You cannot assume that your BC will alone will be enough to manage or transfer ownership of foreign real estate.

In many cases, it is best to have a separate will for property in another country. This step can help avoid legal conflicts, delays, or extra costs for your heirs. Making a local will ensures your property is dealt with under the laws of the country where it is located.

You should always check if your BC will meets the legal requirements for the country your property is in. Some countries may not recognize a will that was made in another place, or may require specific forms and procedures.

Land Ownership Laws in Other Provinces

If you own real estate in another Canadian province, each province has its own rules about how land is inherited and who can act as the executor. The probate process may be different from that in BC, and your executor may have to get special certificates or pay extra fees.

Some provinces require a "resealed grant of probate" before your BC executor can handle property there. This means your will must go through a court process in both BC and the other province. You may also face extra taxes or costs, depending on local regulations.

Handling Foreign Bank Accounts and Investments

Foreign bank accounts and international investments have strict reporting rules for Canadians. Proper management ensures your estate plan, finances, and taxes stay compliant with Canadian law.

Accessing Overseas Financial Accounts

If you have a bank account outside of Canada, you must report any combined value over CAD $100,000 to the Canada Revenue Agency. Assets covered include foreign cash, savings, and securities, even if held through a Canadian financial institution.

Access to foreign accounts may involve extra legal steps, especially after death or incapacity. Prepare by keeping account documentation updated and giving a trusted representative limited legal authority, often through a power of attorney. Without clear instructions, your executor could face major delays or legal hurdles trying to recover or transfer these funds.

Every year, you must file Form T1135 with your Canadian tax return to declare the existence of these accounts and report any income they generate. Failing to meet these obligations can result in significant penalties and tax complications. For specific CRA guidelines on what counts as “specified foreign property”, refer to this explanation on foreign reporting requirements.

Managing International Investment Portfolios

International investments, including stocks, real estate, and foreign mutual funds, fall under Canadian tax scrutiny. The same CAD $100,000 threshold applies, triggering mandatory disclosure and forms with detailed breakdowns of each asset’s income and location.

Keep good records of all transactions, values, and sources of income related to these investments. This helps your estate executor manage compliance and transfer these holdings smoothly upon your death. List accounts, statement details, and contact information for institutions in your estate documents.

Tax rules and forms may change if you own property in multiple countries or if tax treaties are involved.

Updating and Reviewing Wills for Changing Circumstances

Significant life changes can affect your will and estate plans. It is important to keep your documents current to ensure your wishes are respected and your assets are distributed as intended.

Impact of Relocation or Asset Transfer

Relocating to a new province or country can change how your will is interpreted. Each jurisdiction has its own laws regarding wills, taxes, and asset distribution.

Moving outside of British Columbia may mean your will is no longer valid or enforceable as written.

If you acquire property or other assets in a different province or country, local laws could take precedence over your BC will.

Transferring or changing ownership of assets may also have an impact. For example, turning an individual account into a joint account with right of survivorship can change the way that asset is transferred upon your death. Updating your will after an asset transfer is essential to avoid confusion or legal disputes.

Periodic Review Recommendations

Regular reviews of your will help keep your estate plan up-to-date. Life events such as marriage, divorce, the birth of a child, or significant changes in your financial situation are good reasons to review your documents.

It is recommended to review your will at least every three to five years, even if no major events have happened. This helps you make sure that your will still reflects your wishes and includes all relevant assets.

When reviewing, create a checklist:

Update names and contact information

Review and list all current assets

Confirm chosen executors and guardians are still appropriate

Check for changes in laws that could affect your estate

Updating regularly protects your estate and helps prevent disputes amongst your beneficiaries.

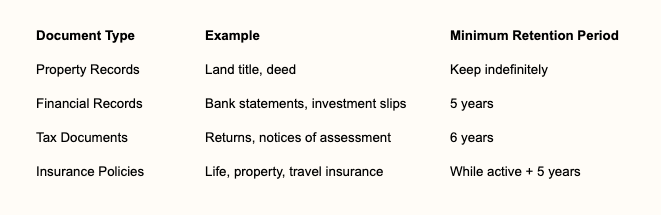

Record-Keeping and Documentation Best Practices

When planning your will, keeping clear and organised records is essential. This helps prevent confusion about your assets, especially those held outside of British Columbia.

Important documents to keep include:

Property deeds and land titles

Bank and investment statements

Insurance policies

Trust agreements

Tax records

Store both physical and digital copies in a secure location. Inform your executor or a trusted person about where these records are kept.

Your records should be accurate, up-to-date, and easy to access. Regularly update your files when assets are sold, acquired, or moved. Following best practices for records management in British Columbia can make the process easier.

For cross-border or international assets, include documentation from each country or jurisdiction. Note any specific requirements or rules for those regions. In Canada, the retention period for most business and financial records is at least five years.

Review your records each year to ensure they reflect your current wishes and asset locations.

Digital Assets Held Outside of BC

Digital assets, such as online bank accounts, email services, and social media profiles, often cross international borders. If you have digital assets stored outside of British Columbia, you will need to plan for them separately from assets inside the province.

You should keep a clear inventory of your digital assets and note which ones are held in other countries. Examples include:

Foreign cryptocurrency wallets

International cloud storage accounts

Social media platforms based outside Canada

Email accounts with foreign providers

Accessing digital assets may require passwords, two-factor authentication, or proof of your death. Some global service providers offer special legacy or account transfer programs that handle accounts after death.

Privacy regulations in other countries may limit your executor’s ability to access or transfer your digital assets. It is important to include clear instructions in your will about who can manage these accounts and where they are held.

A simple digital asset checklist can help you organize:

Legal advice in both BC and the jurisdiction where your digital assets are held may be needed. This will help ensure all rules are followed and your wishes are respected.

Succession Planning for Business Interests Abroad

When you own business assets in another country, you may face local inheritance laws or foreign succession taxes. For example, some countries have forced heirship rules or higher taxes on business transfers.

If you want efficient succession, you may set up separate wills for your foreign and domestic assets. This can help streamline probate and reduce administrative delays.

Consider these steps for planning your business succession across borders:

Identify where each business interest is held.

Understand local laws and tax rules.

Consult a local lawyer in each jurisdiction.

Create separate wills if advised.

Proper advance planning protects your wishes and helps limit costly legal or tax surprises for your heirs.

The Final Verdict

Managing assets located outside of BC requires thoughtful will planning to navigate differing legal systems and ensure your estate is distributed according to your intentions. A well-structured estate plan can reduce administrative hurdles and protect your beneficiaries from unnecessary complications.

To ensure your will is properly drafted and legally sound across multiple jurisdictions, contact the lawyers at Parr Business Law. Our team can help you develop a clear and effective plan tailored to your cross-border estate needs.